We are now seven years past the worst of the housing crisis and the Great Recession of 2008. In most markets, the long foreclosure overhangs and short sales are finally back to historical levels. Hotter markets such as San Francisco, Seattle, Denver, and Dallas are well past their old bubble highs (harder hit markets like Detroit and Las Vegas have a way to go).

However, just as we finally seem to be on the road to recovery, the pessimists are calling for another major crash! What is their reasoning? How could it happen?

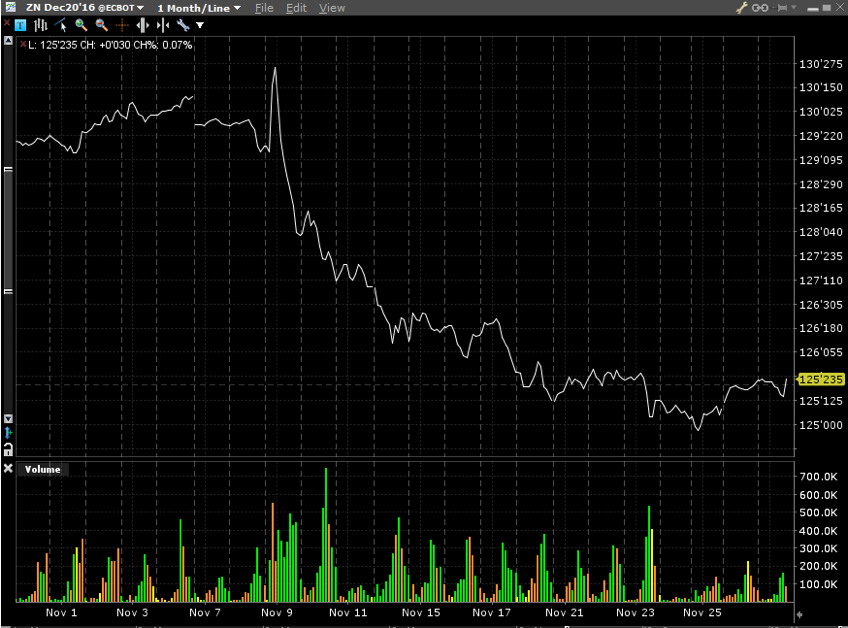

1.) Interest rates are (finally) rising

No one expected the zero-rate environment to last so long. Experts have been calling this one for at least five years (remember when S&P downgraded the US credit rating?). Nevertheless, we are finally seeing a sharp rise in long-term rates irecent n years, coupled with the Federal Funds rate rising, as well as a president-elect that promises to stimulate the economy (with policies likely to bring short-term inflation).

Higher rates mean mortgages are more expensive. Higher mortgages mean less buying power, and less buying power means less competitive bidding for homes.

2.) Crucial tax deductions are in limbo

Investors hate uncertainty, and right now, the upcoming tax policy impacting real estate is one huge question mark. Real estate investors today receive incredibly generous tax breaks. Mortgage interest and real estate taxes are generally deductible when computing income tax. Investors depreciate buildings even though the properties are usually increasing in market value. The more adventurous and frequent flippers benefit from 1031 tax-deferred exchanges and the primary residence capital gains exclusion rules.

The President-elect has vowed to eliminate many tax loopholes in favor of an across-the-board lower income tax rate for everyone. However, Trump has also stressed the importance of home ownership and has undoubtedly taken advantage of many of the real estate tax breaks in his former mogul life. Ultimately, the answer is we don’t know which tax deductions will survive. But the uncertainty itself presents a huge problem as investors take a wait-and-see approach before their next purchase.

3.) Foreign buyers taking a pause

On a related note, it’s no secret forthat eign buyers have played a significant role in the housing recovery since 2008. Some recent trends are dissuading foreign demand. First, the immigration laws are in limbo while the new administration figures out how strictly it wants to pursue isolationist policies. Secondly, several key currencies have been crashing against the USD, making the foreign buying community less attracted to American properties (RMB for example fell 10% in the last 18 months).

Learn more:

4.) The Airbnb arbitrage may be fading

We all love the sharing economy. Many of us have personally benefited from staying as an Airbnb guest or even earning supplemental income as an Airbnb host. What we don’t realize is how much of the total sharing economy is a short-term renting economy. Specifically, there exist many markets where it is very profitable to buy a home, furnish it, arrange regular cleanings, and then rent it out through a short-term rental service. The net income can significantly exceed that of a traditional long-term rental landlord, and the result is upward pressure on housing prices for the entire neighborhood.

We are finally seeing cities fight back. New York City, the largest apartment rental market in the US, has recently passed laws to forbid professional Airbnb hosts from operating without jumping through costly hurdles. Other cities are likely to follow, and in the coming years, we will see one of the most spectacular regulatory debates impacting residents nationwide. The results will impact other companies such as the hotel and hospitality industry. Even online portals, such as RentHop, list longer-term apartments for rent. While we don’t expect Airbnb to vanish, real estate investors may slow down in the coming years as they wait out the legislative and enforcement uncertainty.

5.) The nine-year recession cycle

Let’s go back to the most recent period of extremely high interest rates. In 1981, inflation had run wild. The Volcker-era Federal Reserve fought hard to maintain price stability, employing brutally tight monetary policies that led to 18% interest rates on 30-year mortgages. Fast forward 9 years, and we hit the 1990 oil shock recession (reaching 7.8% unemployment). Most of us have heard of the next downturn, the infamous dot-com bubble that peaked in 1999.

And, of course, the recent housing crisis is fresh on everyone’s mind. In the worst crash since the Great Depression, the stock market fell 60% from its peak to its trough from early 2008 to March 2009. Perhaps it is all a coincidence, but there are compelling arguments that the modern economy is constantly oscillating between boom and bust cycles as capital flows across asset classes. Are we doomed to begin another recession in the next 18 months?

Editor’s Note: We updated this article to enhance readability.