Here is an age old discussion that should have no correct answer. In 2020, whether you are purchasing or refinancing, do you want to lock in record low fixed rate, or go for the one of those 5/1 and 7/1 ARM mortgages?

The Boilerplate Answers

We can give all of the usual “it depends” answers. Do you plan to live in that condo for the rest of your life? Or will you move out once you start a family? Will you try your hand at becoming a landlord and keep the property long after you trade up?

How About A Real Answer?

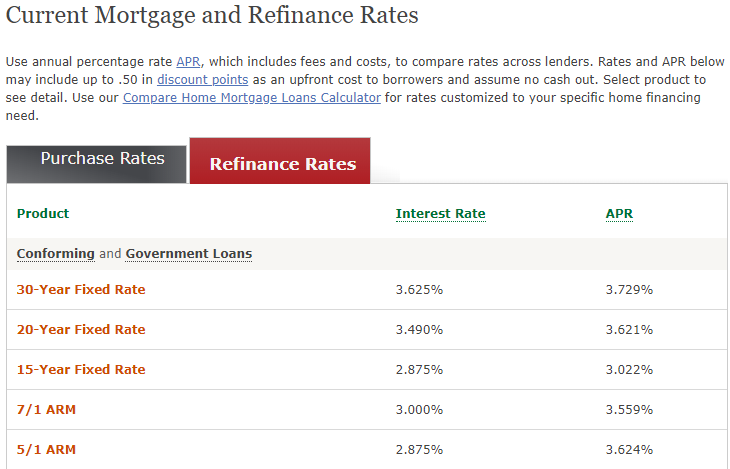

Here is a real answer. Currently in 2020, the spread between a 30-year Fixed and a 7/1 ARM about 0.500%. That’s not a bad deal – truth is, data shows VERY few people actually keep the mortgage longer than seven years. You will either refinance or sell the property by then, or just prepay voluntarily because your financial situation has changed.

Even if you do hit the seven year mark, which I have on my oldest properties, your new rate might not be so horrible. They build in a nice margin over LIBOR, so unfortunately you probably won’t get anything lower than the initial seven year teaser. But it might not be any higher.

And if for some reason your rate skyrockets, you still banked seven years of savings. You would need to hold the higher rate for two to three years before those savings vanished. The real breakeven might be ten years on a 7/1 ARM, in nominal terms. And trust me, by then, your life situation will have changed drastically – you might not even care. In the end, it’s all about peace of mind; sometimes I wish there was no choice and everyone just offered an identical product (in theory they should, thanks to Fannie And Freddie, but some banks sneak in way too many extra fees).

When Is Fixed-Rate Better?

There were moments in the past five years when the Fixed vs ARM mortgage was actually equal! That sounds weird, but the yield curve was just totally flat at the time. For those who really aren’t sure about their future plans, if the 7/1 ARM and 30-year Fixed only have a spread of 0.250%, it’s probably not worth it. You can buy the peace of mind and pay more – just don’t have regrets when you refinance three years later! It’s a calculated gamble.

Editor’s Note: We updated this article to enhance readability.